Stripe's $1 Billion Bet on Bridge: Is It Worth?

(中文在下)

In a bold move that signals a major shift in the fintech landscape, Stripe has announced a $1.1 billion acquisition of Bridge, a web3 infrastructure company specializing in stablecoin orchestration and issuance. This acquisition marks not just Stripe's return to cryptocurrency, but potentially a transformation in how global payments and treasury management operate. Let's dive deep into what this means for the future of financial infrastructure.

Let’s First Look at the Problems Bridge Aims to Solve

Local Currency Limitations: Many countries struggle with unstable economies and hyperinflation, leaving their citizens unable to protect their savings or participate fully in the global economy.

Cumbersome Currency Exchange: Traditional forex solutions remain slow, expensive, and often inaccessible to many users, with existing alternatives frequently adding more costs than solutions.

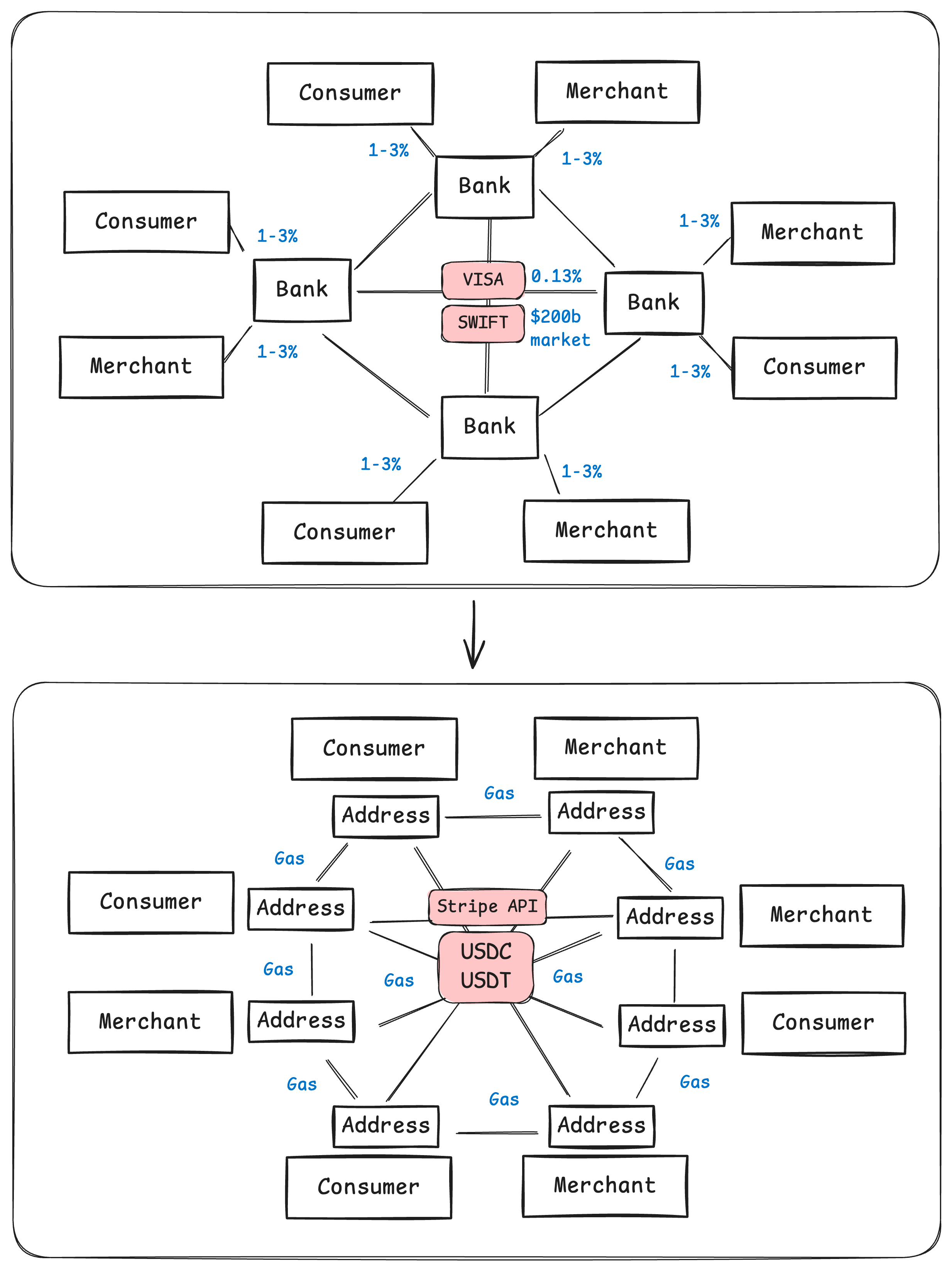

Expensive Cross-Border Payments: Businesses face steep fees (3-4%) and long settlement times for international transactions, creating significant operational overhead.

Bridge has developed a comprehensive stack of solutions

Stablecoin Orchestration: APIs enabling seamless conversion between various dollar formats (USD, EUR, USDC, PYUSD, USDT)

Custom Stablecoin Issuance: Allowing developers to convert supported dollar formats into customizable stablecoin

How Bridge is Making a Real-World Impact?

Payout: Bridge partners with the US government, aid organizations, and creator platforms to distribute payments efficiently via stablecoins. One example is partnering with AIRTM to build payment infrastructure for stablecoin-based payouts to thousands of end-users on aid and gig platforms.

Cross-Border Payments: Bridge enables B2B cross-border payments via stablecoins, partnering with companies like Bitso in Latin America. This allows businesses to make payments between Mexican Pesos (MXN) and USD with fast settlement times (minutes) and lower costs compared to traditional systems like SWIFT.

Dollar Access: Bridge collaborates with fintech companies like Chipper Cash and Dolar App to give consumers in Africa and Latin America the ability to save and spend in US Dollars.

FX: Bridge assists large global companies in repatriating funds earned in Latin America or Africa back to the US, using stablecoins to achieve significantly faster settlement times (under 30 minutes) compared to traditional payment rails.

Now Let’s Turn to Stripe: They have been experimenting with crypto since the early days

Early Adoption and Subsequent Withdrawal: Stripe previously supported Bitcoin payments but discontinued this service in 2018 due to Bitcoin's volatility, slow transaction speeds, and high fees.

Re-entry into Crypto with Stablecoins: After a six-year hiatus, Stripe re-entered the cryptocurrency market in 2024 by allowing businesses to accept USDC payments. This move signals a strategic shift towards stablecoins, which offer price stability and faster transaction speeds compared to Bitcoin.

Stripe's Evolution as a Financial Infrastructure Provider

Stripe has evolved from a simple payment facilitator to "Financial Infrastructure for the Internet" that helps

Simplifies business incorporation process for startups.

Merchants take payments through multiple interfaces and currencies.

Provides robust fraud prevention and risk management protection.

Accelerates payment processing to improve cash flow.

Offers flexible business financing options for growth.

Delivers comprehensive financial management tools for better business insights.

Enables revenue diversification through banking and card issuing services.

What Synergies is Stripe Eyeing with Bridge?

Take Payment: Expand payment options beyond USDC by connecting to various stablecoins across different chains through bridges.

Get paid faster: Reduce payment processing time from days to minutes, which can improve merchant cash flow management, aligning with Stripe's focus on operational efficiency.

Managing cross-currency treasury: Can help Stripe provide merchants with more sophisticated and automated fund management solutions, enabling faster and cheaper settlements, reducing FX volatility risks, especially for businesses involved in complex international transactions.

Is Stripe's $1 Billion Acquisition of Bridge Justified?

Currently, for a credit card payment, merchants need to pay 1.5% to 3% to banks and card network companies. By using stablecoins for settlement, they could potentially save on interchange fees and acquiring bank fees. Stripe's yearly processed payment volume is projected to be $1 trillion in 2023. A 1% fee on $1 trillion amounts to approximately $10 billion.

The global market for international payments is substantial, with total revenues estimated at around $200 billion annually for banks. This includes transaction fees ($10-$50 per transaction) and foreign exchange revenues (1%-5% of transaction volume, depending on the FX pairs). Additionally, banks can earn interest on funds during the transfer process.

According to these data, stablecoins can help merchants save $10 billion annually just from Stripe's own transaction volume. Additionally, crypto can assist Stripe in competing in the $200 billion B2B cross-border payment market with banks. This suggests that the impact of stablecoins could be very significant. If stablecoins can replace traditional banks and card network companies, it becomes clear why Stripe is willing to spend $1.1 billion to acquire Bridge.

Also Stripe's acquisition shows they believe the time is right. Consumers and merchants are becoming more open to using crypto for global settlements.

DeFi has found its product-market fit; now it just needs a good distribution channel.

Stripe is eating banks, as usual, this time through crypto.

10月21日 Stripe 宣布以 11 億美元收購專門從事穩定幣支付和發行的公司 Bridge。這次收購不僅標誌著 Stripe 重返加密貨幣領域,還可能徹底改變全球支付和資金管理的運作方式。

Bridge 想要解決什麼問題?

新興市場法幣波動大:許多新興國家面臨經濟不穩定和惡性通貨膨脹的問題,導致其公民的儲蓄持續貶值或很難參與全球金融服務。

無效率的貨幣兌換:傳統的外匯解決方案仍然緩慢、昂貴,且常常對許多用戶來說難以使用,現有的替代方案往往增加了更多成本而非解決方案。

昂貴的跨境支付:企業在進行國際交易時面臨高額費用(3-4%)和較長的結算時間,造成重大的運營成本。

Bridge 的產品

Bridge 開發了一套全面的解決方案來應對這些挑戰:

穩定幣的轉換:提供 API,實現各種法幣與穩定幣(USD、EUR、USDC、PYUSD、USDT)、各種區塊鏈之間的無縫轉換

自定義穩定幣發行:允許開發者將支持的穩定幣轉換為可定制的穩定幣

Bridge 的使用案例

薪水發放:Bridge 與美國政府、援助組織和創作者平台合作,通過穩定幣分發薪水。與 AIRTM 合作建立支付基礎設施,為援助和零工平台上的數千名終端用戶提供基於穩定幣的支付

跨境支付:Bridge 通過穩定幣實現 B2B 跨境支付,與拉丁美洲的 Bitso 等公司合作,使企業能夠在墨西哥比索(MXN)和美元之間進行支付,結算時間快(分鐘級)且成本低於 SWIFT

美元使用:Bridge 與 Chipper Cash 和 Dolar App 等金融科技公司合作,讓非洲和拉丁美洲的消費者能夠以美元存款和消費。

外匯交易:協助大型跨國公司將在拉丁美洲或非洲賺取的資金匯回美國,SpaceX 也用 Bridge 來做跨國資金管理。使用穩定幣實現顯著更快的結算時間(不到 30 分鐘),相比傳統支付渠道更有效率。

Stripe 很早就開始對 Crypto 的嘗試

Stripe 之前支持過比特幣支付,但由於比特幣的波動性、緩慢的交易速度和高額費用,在 2018 年停止了這項服務。經過六年的暫停後,Stripe 於 2024 年重新進入加密貨幣市場,允許企業接受 USDC 支付,這一舉動顯示了向穩定幣戰略轉移,相比比特幣提供價格穩定性和更快的交易速度。

而 Stripe 早已從簡單的 “收單行” 發展為"互聯網的金融基礎設施"

這張圖很好展現了現在 Stripe 對於其客戶的 Value Proposition 已經拓展到許多方面:

Simplify Incorporation: 簡化初創企業的公司註冊流程

Take Payments: 商戶通過多個界面和貨幣接受支付

Fraud Prevention: 提供強大的欺詐防範和風險管理保護

Get Paid Faster: 加快支付處理以改善現金流

Get Financed: 為業務增長提供靈活的融資選擇

Business Insight: 提供全面的財務管理工具以獲得更好的業務洞察

Diversify Revenue: 通過銀行業務和發卡服務幫助商家實現收入多元化

Stripe 可以透過 Bridge 加強其原本對客戶的 Value Proposition

Take Payments:增加收款選項,不只是USDC,而是透過 Bridge 接上不同鏈上的各種穩定幣。

Get Paid Faster:將支付處理時間從天縮短到分鐘,也可以改善商戶現金流管理,與 Stripe 專注於運營效率的理念一致。

Treasury Management:可能幫助 Stripe 為商戶提供更複雜和自動化的資金管理解決方案,實現更快速、更便宜的結算、降低匯率波動風險,特別是對於涉及複雜國際交易的企業

Stripe 收購 Bridge 的 11 億美元投資是否合理?

目前,商家用信用卡收款需要向發卡行、收單行和 Visa 支付 1.5% 到 3% 的費用,通過使用穩定幣進行結算,可以節省一部分這些份用,Stripe 在 2023 年的支付處理量達到 1 兆美元,只用 1% 費用計算就能省下 100 億美元。

另外全球國際支付市場規模相當可觀,銀行年總收入估計約 2000 億美元,其中包括匯費(每筆交易 10-50 美元)、外匯收入(交易量的 1%-5%,取決於外匯對),銀行還可在轉賬過程中賺取利息。

根據這些數據,穩定幣通過消除給發卡公司和銀行費用,光是 Stripe 自己的交易量,每年可以幫助店家節省 100 億美元,還能夠幫助 Stripe 與銀行競爭 B2B 跨境支付 2000 億美元市場,這意味著穩定幣的影響可能會非常巨大。如果穩定幣能夠取代傳統銀行和 Card Network Company,就能夠理解為何 Stripe 願意花 11 億美元併購 Bridge。

另外 Stripe 的收購也表明他們認為時機已經成熟,消費者和商戶越來越接受使用加密貨幣進行全球結算。DeFi 已找到 PMF,現在只需要一個好的分銷渠道,而現在看來 Stripe 將大大加速這個新的 Paradigm Shift。

Stripe is eating banks, as usual, this time through crypto.